IRA investments should line up with your time horizon, goals, and risk tolerance. If you are a patient investor who doesn’t need to touch that IRA for 20 years, invest accordingly. You can buy funds with high long-term return potential and not worry about the bumps along the way.

If you are closer to tapping that IRA, then taxable bonds and other more conservative investments probably fit the bill. You should also consider asset location. Use more tax-efficient options for your taxable accounts and less tax-efficient for your IRA.

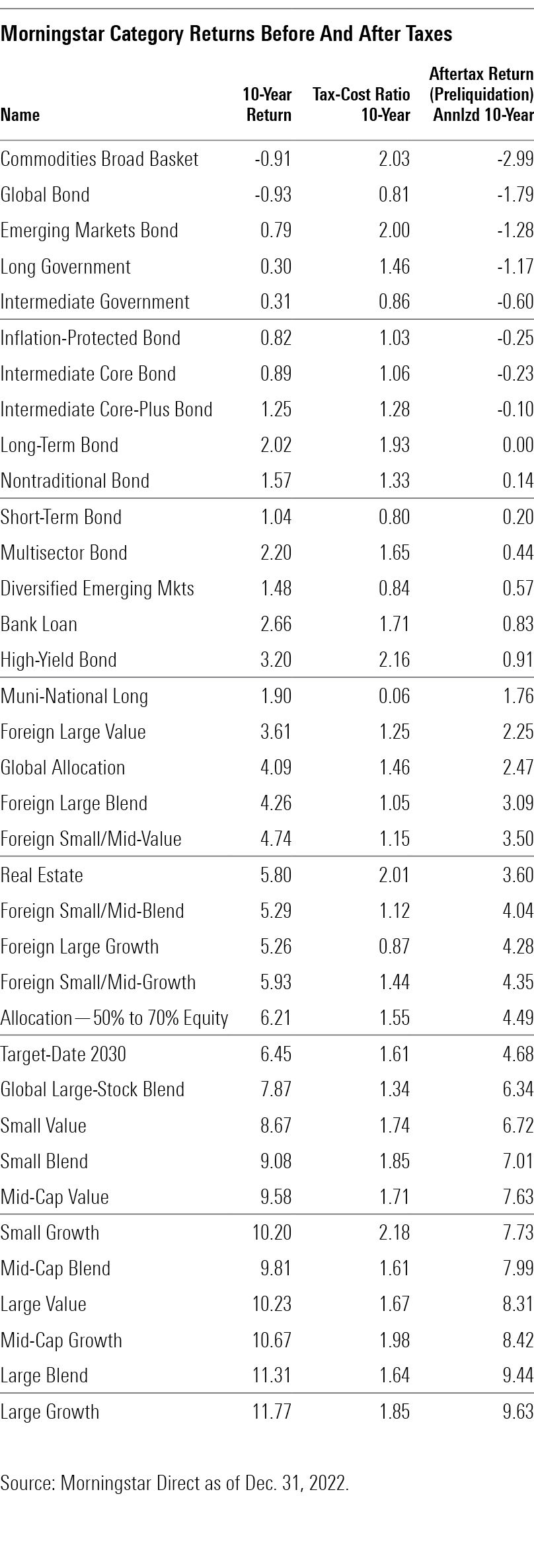

To help you see the big picture, I’ve included a table showing the 10-year tax-cost ratio and aftertax 10-year return of various categories. The tax-cost ratio tells you how much you paid in taxes if you held a fund in a taxable account and were in the highest tax bracket. It’s expressed in basis points (or hundredths of a percent) just like returns and expense ratios.

The tax-cost ratio reflects the funds’ total returns, capital gains distributions, and dividends paid to you. The taxable income part of the equation remains fairly consistent, but the capital gains amount can vary quite a bit. Naturally, a long period of returns can lead to higher taxes, but that’s not such a bad thing because you likely also enjoyed higher aftertax returns.

The 10-year aftertax figure shown here is your return after you paid taxes on income and capital gains, but it does not factor in taxes after you sell the fund. In the table, I ranked categories by low aftertax return rather than tax-cost ratio because funds with low returns after taxes need the most protection from taxes. However, as noted above, that doesn’t mean these funds should constitute most of your IRA holdings as you are aiming for strong returns rather than protection from tax-inefficient investments.

As you can see from the table, seven bond Morningstar Categories had negative 10-year aftertax returns. That partly reflects not only the inefficient nature of their strategies but also that the long-running bond rally turned into a dumpster fire in 2022. It’s likely that the next 10 years will be much better.

On the flip side, U.S. equity categories produced excellent aftertax returns even though they had sizable tax-cost ratios. If returns come down, tax-cost ratios will likely come down, too. And given the current bear market, equity funds will likely have smaller capital gains payouts for the next couple of years.

I’ll review how some categories fit with IRAs and share some suitable funds for those roles.

The Best Bond Fund Types for IRAs

Even in a better return environment, taxable-bond funds are going to be rather tax-inefficient because they throw off steady, taxable income streams. So, it makes sense to hold most of them in tax-sheltered accounts. Inflation-protected bonds are at the top of the list. They adjust based on changes in the rate of inflation, which is a great diversifier if you own a lot of inflation-vulnerable investments like traditional bonds. But the IRS taxes those upward adjustments right away, which eats into their yields.

For Treasury Inflation-Protected Securities, I like Vanguard Short-Term Inflation-Protected Securities Index VTAPX because it has inflation protection but not the interest-rate risk you get with most TIPS funds because its holdings don’t have long maturities. For a core taxable fund, Baird Aggregate Bond BAGIX is a well-run conservative option that pairs well with a high-yield or multisector fund.

A more aggressive option is Fidelity Total Bond FTBFX, where Ford O’Neil can add up to 20% in non-investment-grade bonds, including high yield and emerging markets. If you don’t have a high-yield fund, this is a solid all-in-one option.

High-yield bonds offer the greatest return potential among the fixed-income options, but you realize more of their promise when they’re not taxed. Most other taxable-bond funds also are better off in tax-sheltered accounts, but you may want to own some in taxable accounts for ballast or shorter-term spending needs.

Note that municipal-bond funds are in the middle of the table. They were hurt by rising rates, too, but their tax-sheltered income gives them minuscule tax-cost ratios. These funds belong in your taxable accounts.

The Best Real Estate Fund for IRAs

Real estate funds have a hefty 2.01% tax-cost ratio because much of their returns come from income. They are probably better held in tax-sheltered accounts, but remember that they play niche rather than core roles in portfolios. Also, they are interest-rate sensitive just like intermediate- and long-term bond funds. Vanguard Real Estate Index VGSLX is a low-cost, low-maintenance choice in the sector. It has a Morningstar Analyst Rating of Gold.

Should You Have Allocation Funds in Your IRA?

Allocation categories like 50% to 70% equity and target-date 2030 fall naturally between bonds and equities in the table. While you don’t need an allocation fund in a tax-sheltered vehicle, they provide a couple of big benefits. First, they have smoother returns thanks to their diversification. Admittedly, 2022 showed the limits of that diversification as both equities and bonds sold off, but generally they post modest returns and occasional modest losses. If you tend to react to selloffs by dumping your worst performers, these funds can help you to stay on course.

Second, allocation funds help with rebalancing or, in the case of target-date funds, gradually shifting to fixed income as time goes by. Either way, these funds make investing easier, but because nearly all have taxable-bond portfolios, they are best suited for tax-sheltered accounts.

The Best Equity Funds for IRAs

Actively managed equity funds are more tax-efficient than taxable bonds and balanced funds but less so than index funds. And they suit the long-term goals of most IRA investors, so they make a good choice for the core of your IRA.

Here are four aggressive ideas: Champlain Mid Cap CIPMX is a recently reopened fund where manager Scott Brayman and team have consistently executed a sensible growth strategy and earned a Gold rating. On the value side, there’s Harbor Mid Cap Value HIMVX, a Silver-rated quantitative strategy that generally enjoys a good run when its style is in favor.

T. Rowe Price Global Growth Stock RPGEX also is an excellent growth play. It has a modest asset base and is run by Scott Berg. T. Rowe Price Small-Cap Value PRSVX, where David Wagner looks for financially healthy companies with appealing returns on invested capital, is also worth considering; it straddles the value/blend line and figures to be a long-term winner.

Among less-aggressive equity strategies, I like Gold-rated Vanguard Dividend Growth VDIGX for its high-quality portfolio, moderate risk profile, and super low costs. First Eagle Overseas SGOVX is a risk-averse fund that usually holds up well in down markets while still producing respectable results in rallies. A second foreign gem is American Funds International Growth and Income IGAAX. Capital Group does an excellent job finding foreign dividend payers here while avoiding stocks that offer high yields because they’re so shaky they might blow up.

Should You Include Index Funds in Your IRA?

But what of the most tax-efficient investments? Should you touch index funds in an IRA? Equity index funds align nicely with the main goal of a good long-term investment. If you are starting from scratch, I would suggest putting equity funds in your taxable accounts.

What if you are well along in the process and don’t have any passive funds in your taxable accounts? In that case, equity index funds make sense for your IRA because it’s worthwhile to own them somewhere, and they are consistent with IRA goals for many investors. A good index fund is a dependable low-cost vehicle. And the good core index funds can also help you to raise your core market exposure if you have too many peripheral investments.

So, to that end, consider one of the truly wide-ranging index funds with super low costs: Fidelity Total Market Index FSKAX, which covers the whole United States equity market and charges just 0.02%. Or you can cover the world with a fund like Vanguard Total World Stock Index VTWAX, which charges just 0.10%.

Maximize Your IRA Savings

In 2023, investors 50 or older can contribute a maximum dollar amount of $7,500 to their IRAs, and younger investors can contribute $6,500. While investors have many options for what to put in their IRAs, spending some time thinking about types of accounts and what fits best in them can help you maximize your returns and reach your goals.

This article first appeared in the February 2023 issue of Morningstar FundInvestor. Download a complimentary copy of FundInvestor by visiting this website.